Dealing with the financial hardship that leads to bankruptcy is overwhelming. Adding the legal complexity of selling your Cleveland home on top of it can feel like an impossible burden. You're likely asking yourself: Can I even sell my house? Who is in control of the sale? And what happens to the money?

First, take a breath. Selling a house during bankruptcy in Cleveland is absolutely possible, but it requires following a specific legal process. The path forward depends entirely on whether you're in a Chapter 7 or Chapter 13 bankruptcy, and success hinges on working closely with a knowledgeable bankruptcy attorney.

In 2026, with mortgage rates in the low 6s and ongoing economic pressures, bankruptcy filings are increasing in Cleveland. Many homeowners are discovering they need to sell property as part of their fresh start—and that selling during bankruptcy, while complex, is achievable. This guide will walk you through the process, answer your key questions, and show you how a strategic sale can be the key to moving forward. The process of selling a house during bankruptcy Cleveland homeowners face can be managed with the right partners.

If you're navigating bankruptcy and need to sell your Cleveland home, Home Sweet Home Offers works with bankruptcy attorneys and trustees. Call or text 216-200-8010 for guidance.

Understanding Bankruptcy and Your Cleveland Property

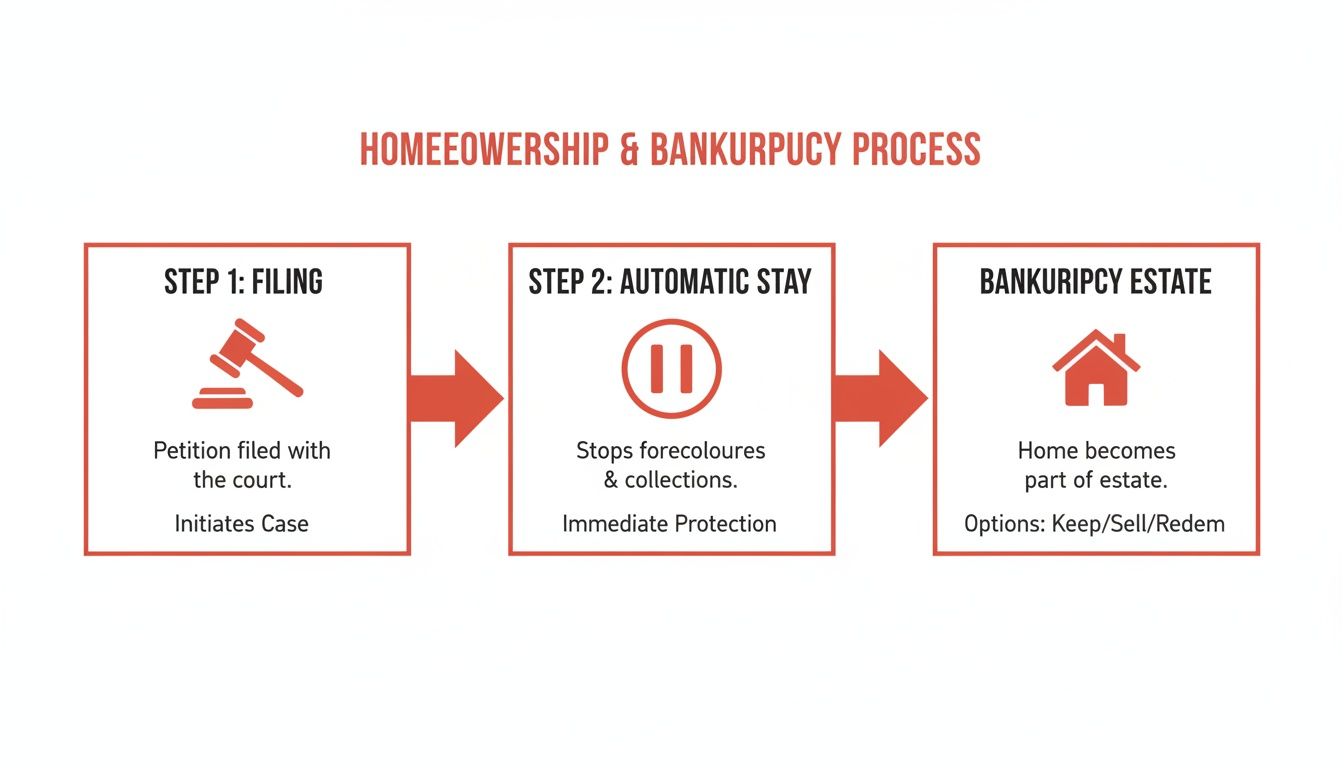

When you file for bankruptcy, two immediate and powerful legal concepts come into play that directly affect your home.

The Automatic Stay

The moment you file, the court issues an Automatic Stay. Think of this as a powerful "pause" button. It immediately stops any active foreclosure sale, halts all collection calls, and prevents creditors from taking further action against you. This provides temporary, but critical, breathing room for you and your attorney to plan the next steps.

The Bankruptcy Estate

Simultaneously, all your property, including your home in Cleveland, Parma, or Euclid, becomes part of what is called the "bankruptcy estate." A court-appointed bankruptcy trustee is given oversight of these assets. This doesn't mean you automatically lose your house, but it does mean you cannot sell it, refinance it, or transfer it without the court's permission.

Chapter 7 vs. Chapter 13: Two Different Paths for Your Home

The fate of your home depends entirely on which type of bankruptcy you file.

- Chapter 7 (Liquidation): This is a faster process, typically lasting 3-6 months. The trustee's job is to sell, or "liquidate," non-exempt assets to pay creditors. Your home may be sold by the trustee if you have equity that exceeds your legal exemptions. However, if your equity is protected, you can often keep the home or get permission to sell it yourself.

- Chapter 13 (Reorganization): This is a 3- to 5-year repayment plan designed to let you keep your property. You make your regular mortgage payments while catching up on arrears through the plan. You retain more control and can choose to sell your property during the plan, but you will still need court approval.

The Ohio Homestead Exemption: Your Key Protection

For Cleveland homeowners, the Ohio Homestead Exemption is the most important tool for protecting your home's value.

- In 2026, this law protects up to $145,425 in home equity for an individual.

- For married couples filing jointly, this amount doubles to $290,850.

If your home's equity is less than this amount, a Chapter 7 trustee will likely "abandon" the property, meaning they won't sell it because there is no value for creditors. Given the property values in many Cleveland neighborhoods, many homeowners find their equity is fully protected, allowing them to either keep their home or sell it and retain the proceeds up to the exemption limit.

Selling Before Filing for Bankruptcy: A Strategic Option

Can you sell your house first and then file for bankruptcy? Yes, but this path requires careful planning and expert legal advice. The bankruptcy trustee has a "look-back" period and will scrutinize all your recent financial transactions, so every move must be transparent and legally sound.

Benefits of Selling Before You File

Selling your home in Parma or Maple Heights before filing can offer significant advantages if done correctly:

- More Control: You manage the sale process without direct court or trustee oversight.

- Simplified Filing: You enter bankruptcy without the complexity of a real estate asset.

- Strategic Use of Proceeds: You can use the sale proceeds to pay off the mortgage and other secured debts, and potentially convert a non-exempt asset (the house) into exempt cash (within your exemption limits).

Risks and the "Look-Back" Period

The bankruptcy trustee has the authority to review your financial history for at least the last two years (sometimes longer). They are specifically looking for:

- Preferential Transfers: Paying back a loan to a family member or friend ahead of other creditors. The trustee can reverse this transaction.

- Fraudulent Transfers: Selling the house for far below market value or giving away the proceeds to hide them.

- Hiding Assets: Failing to disclose the sale and what you did with the money.

Best Practices if You Sell Before Filing

- Consult a Bankruptcy Attorney First: This is non-negotiable. An attorney can advise you on timing and how to handle the proceeds legally.

- Understand Your Exemptions: Know how much cash from the sale you can legally protect.

- Keep Meticulous Records: Document the sale, where the money went, and keep it in a traceable bank account.

- Avoid Unusual Transactions: Don't make large, uncharacteristic purchases or give money away right before filing.

Strategically timing the sale can provide a clean slate. You sell the home, pay off the mortgage, protect your exempt cash, and then file for bankruptcy to discharge remaining unsecured debts.

Considering selling before bankruptcy? Get a cash offer first to know your options. Call 216-200-8010—we work with bankruptcy attorneys regularly.

Selling a House During Chapter 7 Bankruptcy in Cleveland

In a Chapter 7 "liquidation" bankruptcy, the fate of your home is primarily in the hands of the court-appointed trustee. Their job is to evaluate your assets and determine if selling them will generate money for your creditors. When it comes to your house, one of two things will happen.

The Trustee's Role

The trustee will analyze the value of your home, the amount you owe on your mortgage, and your available Ohio Homestead Exemption.

- If your home has significant non-exempt equity (value above the mortgage and your exemption), the trustee will likely move to sell it.

- If your home has little or no non-exempt equity, the trustee will "abandon" the property, as there is no benefit for creditors.

Scenario 1: The Trustee Abandons the Property

This is the most common outcome for Cleveland homeowners. If the trustee abandons your house, control returns to you. You can then file a motion with the court for permission to sell it yourself. This process is straightforward:

- Your attorney files a "Motion to Sell" with the court.

- Creditors are given a 21-day notice period to object.

- Assuming no valid objections, the judge issues an order approving the sale.

- You proceed to closing, and the proceeds (after paying the mortgage) are yours to keep, up to your exemption limit.

Scenario 2: The Trustee Sells the Property

If the trustee decides to sell your home in Lakewood or Bedford, they control the entire process. They will hire a real estate agent or auctioneer and manage the sale. You will have limited input. After the sale:

- The mortgage and any liens are paid off.

- You receive your protected homestead exemption amount in cash.

- The remaining funds are distributed to your creditors.

Why Cash Buyers Are Ideal for Chapter 7 Sales

Whether you or the trustee are selling, a cash offer simplifies everything. Trustees need certainty and speed. A cash offer from a company like Home Sweet Home Offers provides:

- No Financing Contingencies: Eliminates the risk of a buyer's loan falling through.

- A Quick Closing: We can sell quickly and meet court-mandated timelines.

- As-Is Purchase: The trustee doesn't have to worry about making repairs.

This certainty is invaluable, making a cash offer the preferred solution for a smooth, court-approved sale.

Need to sell your Cleveland home during Chapter 7? Cash buyers like Home Sweet Home Offers understand the process and work with trustees. Call 216-200-8010.

Selling a House During Chapter 13 Bankruptcy in Cleveland

Chapter 13 bankruptcy is a "reorganization" designed to help you keep your assets, including your home, while you repay a portion of your debts over a 3- to 5-year plan. But life happens. A job relocation, divorce, or the simple desire to downsize may make selling your home a necessary or desirable step during your plan.

You're in Control, But the Court Has the Final Say

Unlike in Chapter 7, in Chapter 13 you remain in control of your property. You decide if and when to sell. However, you cannot simply put a "For Sale" sign in the yard. Every sale must receive formal court approval to be valid. This process ensures the sale is fair and that the proceeds are handled correctly according to your bankruptcy plan.

The Court Approval Process for a Chapter 13 Sale

Your bankruptcy attorney will guide you through these essential steps:

- File a Motion to Sell: Your attorney files a motion with the bankruptcy court explaining why you need to sell and includes the proposed purchase agreement.

- Notify Parties: The trustee and all your creditors are formally notified and given a 21-day period to raise any objections.

- Court Hearing (If Necessary): Most sales are approved without a hearing if the terms are reasonable. If an objection is filed, a brief hearing may be held for the judge to review the details.

- Court Order and Closing: Once approved, the judge issues an order authorizing the sale. You can then proceed to closing. The entire process, from filing the motion to closing, often takes 6-10 weeks with a motivated cash buyer.

How Sale Proceeds are Handled in Chapter 13

The court order will specify exactly how the money is distributed:

- The mortgage and any other secured liens are paid off first.

- Your Ohio Homestead Exemption is protected and paid directly to you.

- Any remaining, non-exempt proceeds are turned over to the trustee. These funds can be used to pay off your creditors more quickly, potentially allowing you to complete your Chapter 13 plan years ahead of schedule.

Cash Buyers Streamline the Chapter 13 Process

The court approval process requires a certain and reliable buyer. A cash offer provides the court and trustee with confidence that the deal will close on time and without complications from lender financing. This makes the motion to sell much easier to approve, helping you get your fresh start sooner.

Selling during Chapter 13? A cash offer simplifies court approval. Call 216-200-8010 for a no-obligation consultation.

Common Challenges When Selling a House in Bankruptcy

Selling a home during bankruptcy is rarely simple. Life's complexities often add layers of difficulty. Here are some of the most common challenges Cleveland homeowners face and how to navigate them.

Being Underwater on Your Mortgage

When you have an underwater mortgage, you owe more than the home is worth. This complicates a sale significantly.

- The Solution: A short sale, where the lender agrees to accept less than the full mortgage balance, is possible. However, a short sale in bankruptcy requires approval from both the lender and the bankruptcy court, a complex and time-consuming process. Often, surrendering the property in Chapter 7 and having the deficiency debt discharged is a simpler path.

Timing Pressure from Foreclosure

The Automatic Stay provides immediate but temporary relief from foreclosure. If you fall behind on payments during bankruptcy, the lender can ask the court to "lift the stay" and resume the foreclosure process. This creates immense pressure to sell quickly.

- The Solution: A fast cash offer is crucial. We can provide a reliable offer and close on a tight timeline, satisfying the court and lender while preventing the home from being lost at auction.

The Property Needs Major Repairs

Financial hardship often means deferred maintenance. If your home in Garfield Heights needs a new roof or has plumbing issues, you likely don't have the funds for repairs.

- The Solution: Sell your house as-is. Cash buyers like Home Sweet Home Offers purchase properties in any condition. This is ideal for bankruptcy sales, as neither you nor the trustee has the resources or desire to invest in renovations.

Inherited Property During Bankruptcy

If you inherit a house within 180 days of filing for bankruptcy, that inherited property becomes part of the bankruptcy estate. The trustee may seek to sell it to pay your creditors.

- The Solution: Work immediately with your attorney. They can help determine if any exemptions apply and navigate the process of selling the property quickly if required by the trustee.

Dealing with a Rental Property

An investment or rental property is typically a non-exempt asset. In Chapter 7, the trustee will almost certainly sell it. The presence of tenants can complicate a traditional sale.

- The Solution: We buy houses with tenants in place. We can handle the complexities of the lease and tenant communication, making the sale cleaner for the trustee.

Divorce and Bankruptcy Combined

Navigating both Divorce and bankruptcy at the same time is extremely challenging, involving both family court and bankruptcy court. Selling the marital home is often necessary to resolve both cases.

- The Solution: A simple, fast cash sale provides a clear path to liquidating the asset so the proceeds can be divided according to court orders from both legal proceedings.

Facing complications selling during bankruptcy? We've navigated these situations before. Call 216-200-8010 to discuss your specific circumstances.

Working with the Bankruptcy Trustee

The bankruptcy trustee is a central figure in your case. Understanding their role and what they want can make the home-selling process much smoother.

Who is the Trustee?

- Chapter 7 Trustee: This person is appointed to review your finances, identify non-exempt assets, and liquidate them for the benefit of creditors. If your home is being sold, they are in charge of (or must approve) the transaction.

- Chapter 13 Trustee: This trustee's primary role is to administer your repayment plan. They review your major financial decisions, including a home sale, to ensure it complies with your plan and is fair to creditors.

What Trustees Want in a Home Sale

Trustees are fiduciaries responsible for maximizing the value of the estate. When it comes to a real estate sale, they prioritize three things:

- Certainty: Above all, they want a deal that is guaranteed to close. They strongly prefer cash offers because there are no financing contingencies that could cause the sale to fall through at the last minute.

- Fair Value: The property must be sold for a reasonable market price. While they understand the difference between an as-is cash price and a fully renovated retail price, the offer must be justifiable to the court and creditors.

- A Clean Transaction: Trustees prefer simple contracts without complex contingencies. They want to work with professional buyers who understand the bankruptcy process and can provide necessary documentation quickly.

How to Work with the Trustee

- Communicate Through Your Attorney: All communication and negotiation with the trustee should be handled by your bankruptcy lawyer. They know the legal language and protocol.

- Be Responsive: Provide any requested information about the property promptly to your attorney so they can pass it along.

- Choose the Right Buyer: Presenting the trustee with a strong, contingency-free cash offer from an experienced buyer like Home Sweet Home Offers makes their job easier and increases the likelihood of a quick approval. We have experience purchasing properties through bankruptcy and know what trustees need to see.

If the trustee "abandons" the property, you regain control over the sale, but you still need court permission. The process is much simpler, but the principles of providing a certain, fair offer remain the same.

The Step-by-Step Process of Selling During Bankruptcy

While the legal details can seem complex, the practical steps for selling your home during bankruptcy follow a clear path. Here is what the process typically looks like.

If Selling During Chapter 7 (After the Trustee Abandons the Property)

- Confirm Abandonment: Your attorney receives official notice from the trustee that they are not administering the property. This usually happens after the 341 Meeting of Creditors.

- Get a Cash Offer: Contact Home Sweet Home Offers at 216-200-8010. We will assess your property and provide a no-obligation, as-is cash offer within 24-48 hours.

- File a Motion to Sell: Your attorney drafts and files a motion with the court, attaching our purchase agreement and outlining how the proceeds will be distributed.

- Wait for Court Approval: A 21-day notice period allows creditors to object. Assuming none do, the judge will issue an order approving the sale. This typically takes 30-45 days.

- Close the Sale: With the court order in hand, we can close the transaction. The title company will distribute the funds exactly as directed by the court, paying off your mortgage and giving you your exempt proceeds.

If Selling During Chapter 13

- Discuss with Your Attorney: First, talk to your lawyer about why you want to sell and how it will impact your repayment plan.

- Get a Cash Offer: Call us at 216-200-8010 for a firm cash offer that you can present to your attorney.

- Follow the Court Process: Your attorney will file the Motion to Sell. The process of notice, approval, and a court order is similar to Chapter 7 and generally takes 30-45 days.

- Close and Settle: After closing, the proceeds are distributed per the court order. The funds may pay off your plan early, allowing you to exit bankruptcy ahead of schedule and move forward with a true fresh start.

Timeline Summary:

- Chapter 7 (Abandoned Property Sale): 45-75 days from the trustee's decision to closing.

- Chapter 7 (Trustee Sale): 3-6 months.

- Chapter 13 (Your Sale): 45-90 days from getting an offer to closing.

Ready to start the process? Call 216-200-8010 for a no-obligation cash offer you can take to your bankruptcy attorney.

Understanding Costs and How Proceeds Are Distributed

When your house is sold during bankruptcy, the money doesn't just go into your pocket. It's distributed in a specific order, as dictated by law and the court. Here’s a clear breakdown of where the money goes.

What Comes Out of the Sale Proceeds First

- First Mortgage: Your primary mortgage lender is first in line and must be paid in full at closing to provide a clear title to the new buyer.

- Other Secured Liens: Any other debts attached to the property are paid next. This includes second mortgages, HELOCs, property tax liens, or judgment liens.

- Closing Costs: Standard real estate transaction fees like title insurance and recording fees are paid. When you sell to Home Sweet Home Offers, we typically pay all of these closing costs for you.

- Real Estate Commissions (If Applicable): If a real estate agent is involved (common in trustee sales), their commission (usually 5-6%) is paid. By selling directly to a cash buyer, you avoid this cost entirely.

What You Get to Keep: The Ohio Homestead Exemption

After all the debts attached to the property are paid, you receive your protected equity.

- The Ohio Homestead Exemption allows you to keep up to $145,425 (for an individual filer in 2026) or $290,850 (for a married couple). This money is legally shielded from your other creditors.

Example Calculation:

- Sale Price: $180,000

- Mortgage Payoff: -$120,000

- Other Liens: -$5,000

- Closing Costs: $0 (Paid by Home Sweet Home Offers)

- Net Proceeds: $55,000

Since $55,000 is well below the $145,425 exemption, you would keep the entire amount.

What Goes to Creditors

Any proceeds left over after paying off liens and your full homestead exemption go to the bankruptcy trustee. The trustee then distributes this money to your unsecured creditors according to the rules of bankruptcy.

If your home is underwater and sells for less than the mortgage balance, you walk away owing nothing further on the property. The remaining mortgage debt is discharged in your bankruptcy, giving you a complete fresh start.

Frequently Asked Questions

Q: Can I sell my house while in bankruptcy?

A: Yes, but you need court approval. In Chapter 7, the trustee may sell it or abandon it (letting you sell). In Chapter 13, you can sell with court permission. Either way, the process is manageable with proper legal guidance.

Q: Will I get any money from selling during bankruptcy?

A: Usually yes. Ohio's homestead exemption protects up to $145,425 in equity per person. If your equity is less than the exemption, you keep all proceeds after paying the mortgage and liens.

Q: Do I need my bankruptcy attorney involved?

A: Absolutely. Never try to sell property during bankruptcy without attorney involvement. The sale must be properly structured and court-approved. Your attorney files necessary motions and protects your interests.

Q: How long does it take to sell during bankruptcy?

A: Cash sales can close 45-75 days after the decision to sell (including the court approval process). Traditional sales take longer due to financing contingencies and buyer uncertainty.

Q: Can the trustee force me to sell my house?

A: In Chapter 7, if your home equity exceeds your exemption, the trustee may sell it. In Chapter 13, you typically keep your home as long as you make payments. If you want to keep the house, discuss with your attorney immediately after filing.

Q: What if my house needs repairs and I can't afford them?

A: Cash buyers like Home Sweet Home Offers purchase as-is. No repairs are needed. This is actually ideal for bankruptcy situations where you have no money to invest in the property.

Q: Can I sell to a family member during bankruptcy?

A: Extremely risky. Sales to family members are heavily scrutinized and can be reversed as fraudulent transfers. Always sell at fair market value to unrelated buyers.

Q: Will selling affect my bankruptcy discharge?

A: No, selling property properly during bankruptcy doesn't affect your discharge. The sale is part of administering the estate. Your discharge proceeds as normal.

A Clear Path Forward

Selling a house during bankruptcy in Cleveland, while legally detailed, is a well-defined process that can lead to a true financial fresh start. With the court's approval and your attorney's guidance, it is entirely possible. In Chapter 7, the trustee may sell your home, or more commonly, abandon it so you can sell it. In Chapter 13, you remain in control and can choose to sell. In both scenarios, Ohio's generous homestead exemption protects up to $145,425 of your equity per person.

With economic pressures continuing and mortgage rates in the low 6s, more Cleveland homeowners are navigating bankruptcy while needing to sell property. The process works—thousands do it every year.

A direct cash buyer simplifies the entire journey. We provide the certainty that trustees and courts require, purchase your home as-is so you don't need to invest in repairs, and can close on the court's timeline.

Navigating bankruptcy while needing to sell your Cleveland home doesn't have to be overwhelming. Home Sweet Home Offers works regularly with bankruptcy attorneys and trustees—we understand the process and can provide a fast, certain cash offer that makes court approval straightforward. Whether you're in Chapter 7, Chapter 13, or considering bankruptcy, call or text 216-200-8010 for a confidential, no-obligation discussion of your options.

Sources

- U.S. Bankruptcy Code (11 USC)

- Ohio Revised Code (exemptions)

- Northern District of Ohio Bankruptcy Court

- Cuyahoga County Common Pleas Court

- Ohio State Bar Association (bankruptcy resources)

- American Bankruptcy Institute