"Can I even sell my house to a cash buyer if I still owe money on it?"

If you're a Cleveland homeowner thinking about selling, this might be the biggest question on your mind. We hear it all the time, and we're here to give you a clear, reassuring answer: Yes, absolutely. Having a mortgage is normal, and it doesn't stand in the way of a fast, straightforward cash sale. In fact, selling is how most mortgages get paid off.

What Happens to My Mortgage in a Cash Sale?

This guide is designed to pull back the curtain and show you exactly how the process unfolds for homeowners in Cleveland and surrounding areas like Parma, Euclid, and Lakewood. We'll demystify everything, starting with the most important point: your mortgage gets paid off at closing by a professional title company, using the funds from the sale. You don't have to pay it off out-of-pocket beforehand.

From University Heights to Lorain, we talk to local homeowners every day who are weighing their options. In 2026, many are sitting on great 3-4% mortgage rates from a few years ago and are hesitant to give them up. But when life happens—a job relocation, a divorce, or an inherited property that's too much to handle—you need a simple path forward.

Our goal is to clear up the common myths and show you how selling for cash provides a simple, clean solution.

Busting Common Mortgage Myths

Let's tackle some of the biggest misconceptions right out of the gate:

- Myth: "I have to pay my mortgage off before I can sell." (False) The sale itself is what pays off the mortgage. The proceeds from the buyer are used to settle the loan balance at closing.

- Myth: "Cash buyers won't deal with mortgaged properties." (False) At Home Sweet Home Offers, nearly every house we buy has a mortgage. This is a standard, everyday part of our process.

- Myth: "My mortgage company has to approve the buyer." (Usually not) As long as the loan is being paid in full from the sale, your lender doesn't get a say in who buys your house.

- Myth: "I can't sell if I don't have much equity." (Not always) While more equity means more cash in your pocket, it's not always a dealbreaker. We work with homeowners in all kinds of equity situations.

We're here to give you the clear, honest answers you need. We'll walk you through exactly how your mortgage is handled when you decide to sell my house fast Cleveland so you can move on to your next chapter with confidence.

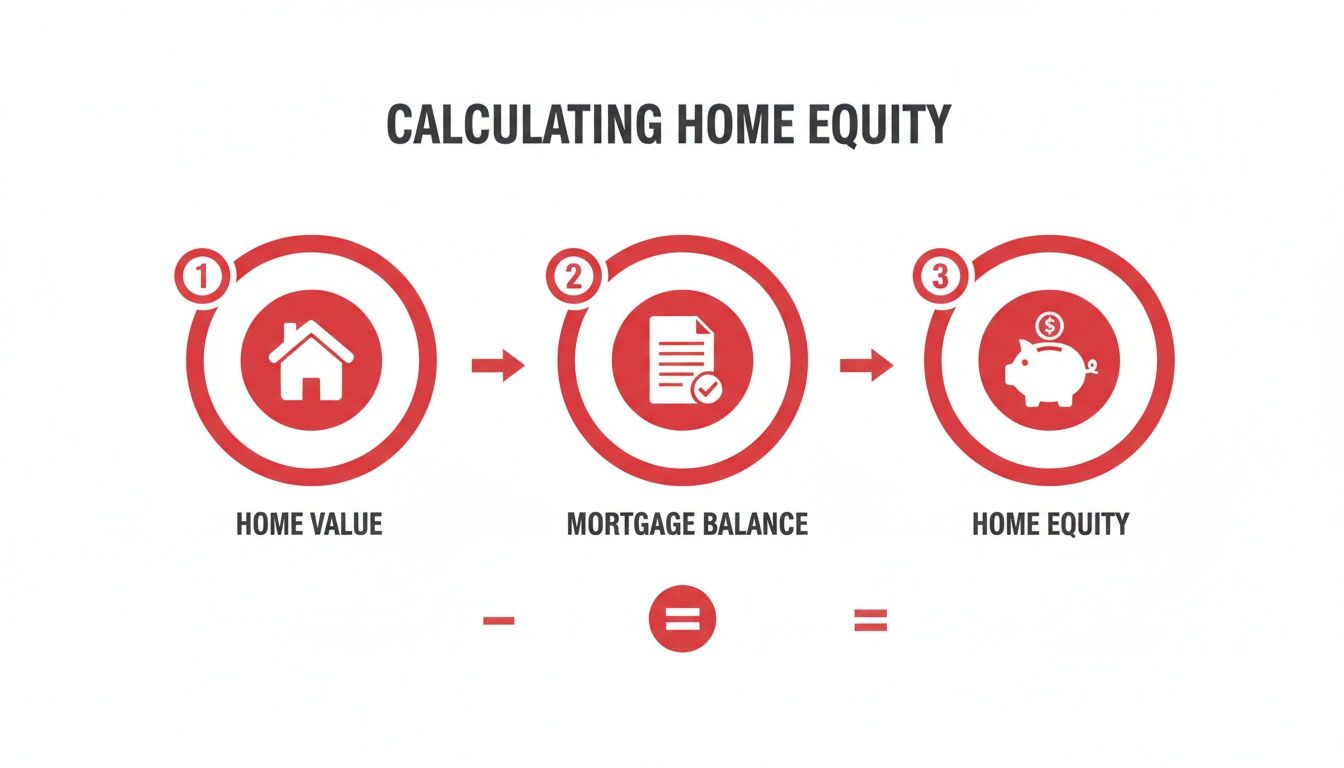

Calculating Your Home Equity and Payoff Amount

Before selling your Cleveland home, you need to get a handle on two key numbers: your mortgage balance (what you still owe) and your home equity (the portion you truly own). The math is simple.

- Home Equity = Your Home's Current Market Value – Your Mortgage Balance

Let's say your house in Garfield Heights or Euclid is worth around $150,000. You check your mortgage statement and see you owe $100,000. The difference—$50,000 in this case—is your home equity. That's the cash you can generally expect to walk away with after the loan is paid off.

However, the balance on your monthly statement isn’t the final figure. To get the exact number, you need an official "payoff quote" from your lender.

Why Your Payoff Quote is Different

Your mortgage accrues interest every single day. The payoff quote is a precise, time-sensitive calculation from your lender that includes:

- Principal Balance: The core amount you still owe.

- Per Diem Interest: This is the daily interest that adds up until the exact day your loan is officially paid in full.

- Fees: Any late fees or other charges on your account.

- Prepayment Penalties: These are rare in modern loans but worth checking for.

A payoff quote is typically valid for about 30 days. The title company handling your sale will request a fresh one right before closing to ensure the final number is perfect.

Understanding Your Equity in the Cleveland Market

In 2026, Cleveland's median home values hover between $120,000 and $140,000. Many homeowners in Parma and Lakewood who bought between 2019 and 2021 have built a solid equity cushion through appreciation. If you bought earlier, you're likely in an even better spot.

On the other hand, if you recently did a cash-out refinance to fund a renovation or pay off debt, your equity might be thinner. In some cases, a homeowner might even be "underwater," meaning they owe more than the home is worth. This can happen with recent purchases or if a property in a neighborhood like Maple Heights needs extensive repairs that lower its value. Understanding your position is the first step toward a predictable sale with Cleveland cash home buyers.

The Step-by-Step Mortgage Payoff Process

So, what really happens behind the scenes after you accept a cash offer? The process is surprisingly organized and handled by professionals, making it straightforward for you. The title company acts as a trusted neutral party, ensuring every dollar goes exactly where it's supposed to.

Here’s a clear look at how it all unfolds.

Days 1-2: Offer Acceptance and Escrow Opening

The moment you sign the purchase agreement with Home Sweet Home Offers, the clock starts. We immediately send the contract to a trusted local title company to formally "open escrow." Escrow is just a secure holding account for all the funds and documents. You'll provide the title company with your mortgage lender's information so they can get the ball rolling.

Days 3-7: Your Payoff Statement Is Ordered

With your loan info, the title company contacts your lender for an official payoff statement. This document is key, spelling out the exact amount needed to clear your loan on a specific date, including principal and per diem interest. While this is happening, the title company also runs a title search to ensure there are no other liens or claims on your property.

Days 7-14: Closing Day and Funds Distribution

Once the title company has the official payoff number and confirms the title is clear, they prepare a final settlement statement. This document breaks down the entire sale.

On closing day, it’s a simple, three-step process:

- Funds Arrive: We wire the full purchase amount into the title company's secure escrow account.

- Mortgage Is Paid: The title company immediately wires the exact payoff amount directly to your mortgage lender, wiping out your debt.

- You Get Paid: The remaining balance—your home equity—is wired to your bank account or issued as a certified check.

This infographic breaks down the simple math at the heart of your sale.

The money you walk away with is simply what your home sold for minus what you owed. For Cleveland sellers who need to sell house fast for cash Cleveland, this clean process cuts out the usual stress and delays.

How to Read Your Settlement Statement

The settlement statement (often called an ALTA statement in Ohio) can look intimidating, but it's just the final receipt for your home sale. It shows exactly where every dollar went, starting with the big number—your sale price—and then listing all the deductions.

The first line you'll see is the gross sale price. This is the full cash offer you agreed to.

Understanding Your Deductions

From that sale price, the title company subtracts all costs needed to close the deal. For a typical Cleveland homeowner, this includes:

- First Mortgage Payoff: The largest deduction, covering your remaining principal and interest.

- Second Mortgage/HELOC: If you have another loan, its full payoff is also deducted.

- Property Tax Proration: You're responsible for property taxes up to the day of sale. This line item settles what you owe.

- Transfer Taxes: In Cuyahoga County, the seller typically pays a transfer tax of about 0.8% of the sale price.

- Title and Closing Fees: Standard charges for the title company’s work.

- HOA Payoffs: Any outstanding dues or fees if you're in a homeowners association.

Example Settlement for a Cleveland Home

Let’s put real numbers to this. Imagine you're selling a home in West Park for $130,000.

- Sale Price: $130,000

Less Deductions:

- First Mortgage Payoff: $85,000

- Property Tax Proration: $800

- Title Insurance (Owner's Policy): $650

- Transfer Tax: $1,040

- Closing Fees: $500

Seller Net Proceeds: $42,010

That final number, "Seller Net Proceeds," is the exact amount of cash coming to you.

How You Get Your Money

One of the best parts of a cash sale is there's no waiting. The buyer's money is already in the title company's escrow account. The moment you sign, the title company can wire your proceeds directly to your bank account, often the same day. This speed is a huge advantage when you need to sell my house fast for cash.

Navigating Special Mortgage Situations

Life is rarely simple, and neither are mortgages. Many homeowners in Cleveland have more than just a single, standard loan. The good news? When you sell your house with a mortgage to a cash buyer in Cleveland, these unique situations are handled smoothly and professionally.

An experienced buyer like Home Sweet Home Offers partners with the title company to sort everything out, ensuring a predictable closing, no matter what your mortgage looks like.

Second Mortgages and HELOCs

If you've tapped into your home's equity with a second mortgage or a Home Equity Line of Credit (HELOC), both loans must be paid off when you sell. The process is the same as for your main mortgage. The title company requests a separate payoff for each lien, and the sale proceeds are used to clear all property-related debt in one go.

FHA, VA, and Reverse Mortgages

Worried that a government-backed loan might complicate a cash sale? Don't be.

- FHA and VA loans follow the same payoff process as conventional mortgages and are prohibited from having prepayment penalties.

- Reverse mortgages (HECMs) are also handled smoothly. We often see these when heirs sell an inherited property in neighborhoods like Bedford or University Heights. The full balance, including principal and all accrued interest, is paid off from the sale proceeds.

Mortgages in Forbearance or with Penalties

If you used a forbearance program to pause payments, those deferred amounts are added to your loan balance. The title company will get an accurate payoff figure from your servicer that includes everything you owe. While rare in loans after 2014, some older mortgages may have prepayment penalties. If yours does, this fee will be listed as a deduction on your settlement statement.

No matter the scenario, a professional cash buyer has seen it all before. We regularly we buy houses Cleveland with every kind of mortgage complexity imaginable, providing a simple solution every time.

How Cash Buyers Differ From Traditional Sales with Mortgages

When you sell to a buyer using a mortgage, the process has extra steps and uncertainties that simply don't exist in a cash sale. For a Cleveland seller with a mortgage, understanding this difference is key.

Traditional Sale with a Financed Buyer

- Financing Delays: The buyer's loan application, underwriting, and approval process can take 30-60 days.

- Appraisal Risk: The buyer's lender requires an appraisal. If it comes in low, the deal can fall apart or force you to lower your price.

- Longer Closing: The extended timeline means you pay more in per diem (daily) mortgage interest while you wait.

- Uncertainty: The buyer's financing could be denied at the last minute, sending you back to square one.

The Home Sweet Home Offers Cash Sale

- No Financing: We use our own funds, so there's no buyer loan process.

- No Appraisal: We do our own valuation. The price we offer is the price you get.

- Speed: We can close in 7-14 days, saving you money on interest and carrying costs.

- Certainty: Once we sign the agreement, the sale is guaranteed. Cash is already secured.

Per Diem Interest Savings Example

Let's say your mortgage balance is $100,000 at 6% interest. Your daily interest is about $16.44.

- Traditional Sale (60 days): You pay an extra $986 in interest while waiting to close.

- Cash Sale (14 days): You only pay $230 in interest.

- Savings: $756

The financial savings are nice, but the certainty and peace of mind that come with a cash sale are priceless for many homeowners. When you work with cash home buyers Cleveland, you eliminate the biggest risks of a traditional sale.

What Happens When You Owe More Than Your Home Is Worth

Let's tackle a tough but crucial topic: negative equity. This happens when your mortgage balance is higher than what your home could sell for, often called being "underwater."

Imagine your house in Parma is valued at $100,000 because it needs significant repairs. However, you still owe $115,000 on your mortgage. The sale price won't cover the loan, leaving you with a $15,000 shortfall. In this situation, a standard sale isn't possible, as the lender won't release their lien on the property until they're paid in full.

Your Options When You’re Underwater

Facing a mortgage shortfall is daunting, but you have options.

-

Bring Cash to Closing: This is the most straightforward solution. If the gap isn’t too large and you have the funds, you can bring a certified check for the difference to closing. In our example, you’d bring $15,000. The title company combines your funds with ours, pays the lender the full $115,000, and the sale is complete.

-

Pursue a Short Sale: When bringing cash isn't an option, a short sale is the next step. You formally ask your lender to accept less than the full amount owed. They often agree because it's a better financial outcome for them than a lengthy foreclosure. The process can take months, which is why lenders often prefer a solid cash offer—there's less risk of the deal falling apart while they make their decision.

-

Deed in Lieu of Foreclosure: This involves voluntarily transferring the property deed to the lender to avoid a foreclosure auction. You should always consult an attorney before choosing this path.

Being underwater is a heavy burden, but you absolutely have a path forward. We can help you understand the best option for your unique circumstances. Check out our guide on navigating an underwater mortgage in Cleveland.

Ready to See Your Cleveland Cash Offer?

Having a mortgage doesn't have to be a barrier to selling your Cleveland home quickly and easily. It's a normal part of the process, and at Home Sweet Home Offers, we're here to make it simple. You get speed, certainty, and a solution that works no matter your property's condition or your financial situation.

We're not a faceless national company; we're right here in Ohio. We understand the local market, from the lakefront in Euclid to the quiet streets of Bedford and Maple Heights. We invite you to get a free, no-pressure cash offer from our team today.

We'll provide a clear, transparent breakdown, showing you exactly how much you can expect to receive after your mortgage is settled. There’s zero obligation, just a straightforward answer from a local team you can trust.

Call us at 216-200-8010 or fill out our online form to get a cash offer now.

Common Questions We Hear About Selling With a Mortgage

Even with a clear process, it's normal to have a few questions. Here are the most common concerns we hear from homeowners in Cleveland.

Do I Need to Ask My Lender for Permission to Sell?

No. You do not need your lender’s permission to sell your home. Your mortgage includes a "due-on-sale" clause, which simply means the loan must be paid in full when you sell. A cash sale handles this requirement perfectly. You have the right to sell your property.

What Happens to the Money in My Escrow Account?

Your lender will mail you a check for any leftover money in your escrow account, usually within 30 days of closing. This money, which you paid for future property taxes and insurance, legally belongs to you. Don't forget to cancel your homeowner's insurance policy after the sale to get a refund for any unused premium.

Can I Sell My House If I'm Behind on Payments?

Yes, absolutely. This is a very common reason people choose to sell to us, especially if they're facing pre-foreclosure in Cuyahoga County. The lender will simply include any overdue payments and late fees in the final payoff quote. As long as the cash offer is high enough to cover that total, the sale can proceed smoothly, protecting your credit from a foreclosure.

Will Paying Off My Mortgage Hurt My Credit Score?

No, it's the opposite. Successfully paying off a large loan like a mortgage is a positive event for your credit history. It shows you met a major financial commitment. The only thing that hurts your credit is missing payments before the sale. A clean payoff is a great mark on your credit report.