Selling a house in Cleveland in 2026 is a huge financial step, and thinking about taxes can feel overwhelming. We understand that whether you're facing foreclosure, managing an inherited property, or just ready for a change, the last thing you want is a surprise tax bill.

The good news is that most Cleveland homeowners who sell their primary residence will pay ZERO federal capital gains tax. Thanks to a generous IRS exclusion, the profit you’ve worked so hard for is often completely protected.

However, understanding your specific situation is key. For homeowners in Cleveland, Parma, Lakewood, and across Northeast Ohio, certain scenarios can trigger tax obligations. This guide is here to walk you through it, step-by-step.

Why You Can't Ignore Taxes When Selling Your Cleveland Home

Getting a handle on your potential tax liability before you sell is the smartest move you can make. It helps you plan strategically and ensures you walk away with the most money possible.

Here are the situations where taxes become a critical factor:

- Rental Properties: If you're a tired landlord in Euclid or Maple Heights, the rules are different. Investment properties don't get the same tax breaks.

- Significant Profits: If your gain is over the generous $250,000 (for single filers) or $500,000 (for married couples) limits, the excess is taxable.

- Short Ownership: If you’ve lived in the home for less than two of the last five years, you may face taxes.

- Inherited Homes: While often tax-friendly, an inherited home in Bedford or Lorain can have complexities, especially for out-of-town heirs.

Understanding these rules before you sell my house fast Cleveland is crucial. This guide will break down federal and Ohio taxes, giving you the clarity to make an informed decision for your family.

Capital Gains Tax Basics for Cleveland Home Sellers

When you sell your home, you're not taxed on the sale price—you're taxed on the profit, which is called a capital gain. Understanding how to calculate this is the first step in determining your tax liability.

The formula is simple:

Sale Price – Cost Basis = Capital Gain

Your cost basis is your total investment in the property. It’s more than just what you paid for it.

- Original Purchase Price: The amount you paid for the home.

- Closing Costs (from purchase): Certain fees you paid when you bought the property.

- Capital Improvements: The cost of major upgrades that add value or extend the life of your home. This is crucial—it's not for routine repairs.

| What's a Capital Improvement? | What's a Repair? (Does NOT count) |

|---|---|

| New Roof ($12,000) | Painting a room |

| Kitchen Remodel ($25,000) | Fixing a plumbing leak |

| Room Addition ($40,000) | Carpet cleaning |

Keeping meticulous records of these improvements directly reduces your taxable gain.

Short-Term vs. Long-Term Capital Gains (2026 Rates)

The amount of time you’ve owned the property determines your tax rate.

- Short-Term (owned less than 1 year): Taxed as ordinary income, at rates from 10% to 37%. This is rare for home sales but can happen in a flip situation.

- Long-Term (owned 1+ years): Taxed at lower, preferential rates of 0%, 15%, or 20%.

2026 Long-Term Capital Gains Tax Brackets (Married Filing Jointly)

- 0% rate: Taxable income up to $94,050

- 15% rate: Taxable income from $94,051 to $583,750

- 20% rate: Taxable income over $583,750

(For single filers, the 15% bracket starts at $47,026 and the 20% bracket starts at $518,901.)

Cleveland Example

Imagine you're a married couple selling a rental property in Garfield Heights.

- Purchased in 2015: $120,000

- Capital Improvements: $35,000

- Your Cost Basis: $155,000

- Sold in 2026: $195,000

- Your Capital Gain: $40,000 ($195,000 – $155,000)

If your total household income is $100,000, that $40,000 gain falls into the 15% bracket.

Federal Tax Owed: $40,000 x 15% = $6,000

However, if this was your primary residence, you would likely owe $0 tax because of the exclusion we'll cover next. Navigating these rules is why many sellers turn to Cleveland cash home buyers for a simple, predictable sale.

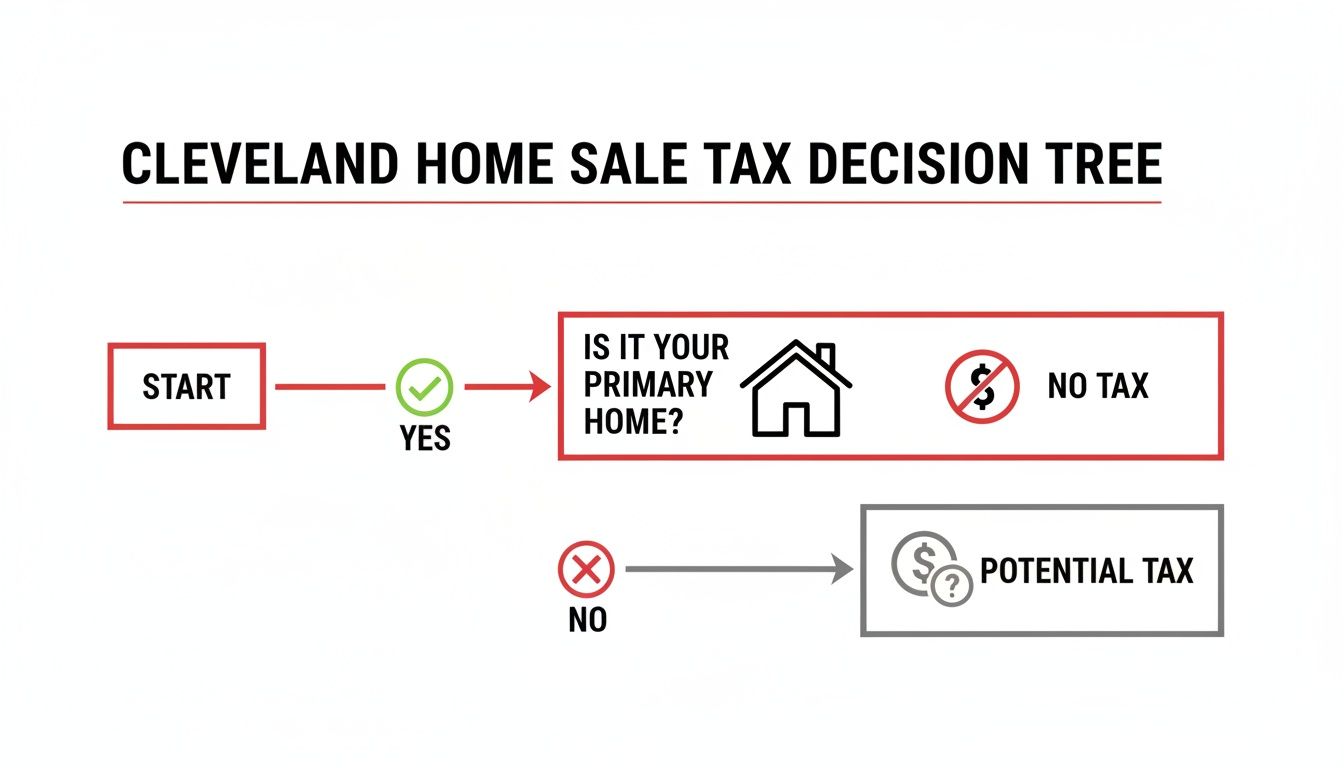

The Primary Residence Exclusion – Your Biggest Tax Break

For homeowners, this is the most important tax rule to know: IRS Section 121. It’s the reason the vast majority of people who sell the home they live in pay zero federal tax on their profit.

We understand that when you're selling due to a job transfer, divorce, or the need to downsize, the last thing you want is a tax burden. This exclusion is designed to protect you.

How the Exclusion Works

The IRS allows you to exclude a massive amount of your profit from your taxable income:

- $250,000 of capital gains for single filers.

- $500,000 of capital gains for married couples filing jointly.

This isn't a deduction; it's a complete exclusion. The government simply treats that profit as if it doesn't exist for tax purposes.

Qualification Requirements

To claim the full exclusion, you must meet two simple tests during the 5-year period before your sale date:

1. The Ownership Test:

- You must have owned the home for at least 2 of the 5 years (24 total months).

- The months don't need to be consecutive.

2. The Use Test:

- You must have lived in the home as your primary residence for at least 2 of the 5 years (24 total months).

- Temporary absences for vacations or work trips still count as time you lived there.

You must meet both tests, and you can only use this exclusion once every two years.

Partial Exclusion Scenarios

Life doesn’t always fit into a neat two-year box. If you have to sell early due to a situation you can't control, you may still qualify for a partial, or prorated, exclusion. Qualifying reasons include:

- Job Relocation: Your new job is 50+ miles farther from your home.

- Health Reasons: A doctor recommends you move for medical care.

- Unforeseen Circumstances: This can include divorce, death of a spouse, job loss, or having twins from a single pregnancy.

The partial exclusion is calculated based on the time you did live there. For example, if a single person lived in their home for 18 months before a qualifying move, they could exclude up to $187,500 of their gain (18/24 x $250,000).

The Cleveland Market Reality

With a median home value around $130,000 in Cleveland, it is extremely rare for a homeowner’s profit to exceed the $250,000/$500,000 limits. Even in hot neighborhoods like Tremont or Ohio City, the average gain of $30,000 to $60,000 for a long-term owner falls comfortably within these tax-free limits. This is why we can confidently say that most Cleveland primary residence sellers owe ZERO federal capital gains tax. Understanding if is now a good time to sell in Cleveland is easier when you know your profit is likely safe from taxes.

Rental and Investment Property Taxes

For tired landlords in Cleveland, Parma, or Elyria, selling an investment property is a different story. The tax rules are stricter and can lead to an unexpected bill if you’re not prepared. We often speak with landlords who are facing costly repairs or problem tenants and just want a simple way out. Understanding the tax implications is the first step.

No Primary Residence Exclusion for Rentals

The biggest difference is that rental properties do not qualify for the $250k/$500k primary residence exclusion. Every dollar of profit you make is potentially taxable. This is where many Cleveland landlords face a surprise tax liability.

Depreciation Recapture – The Hidden Tax

When you own a rental, the IRS allows you to deduct depreciation each year to lower your taxable rental income. It’s a great benefit during ownership. However, when you sell, the IRS wants that tax benefit back.

This is called depreciation recapture. All the depreciation you've claimed over the years is "recaptured" and taxed at a flat rate of up to 25%. This is a separate tax paid in addition to the standard capital gains tax.

Example:

- You bought a Cleveland duplex for $100,000.

- You owned it for 10 years and claimed $29,091 in depreciation.

- You sell it for $150,000.

- Depreciation Recapture Tax: $29,091 x 25% = $7,273

- Remaining Capital Gain: You'd then calculate the regular capital gains tax on the rest of your profit.

- Total Federal Tax: Over $14,000 in this scenario.

Strategies to Minimize Rental Property Taxes

If you're facing a large tax bill from a rental sale, you have options:

- 1031 Exchange: This allows you to defer all capital gains taxes by rolling the proceeds into a new "like-kind" investment property. There are strict deadlines (45 days to identify, 180 days to close), but it’s a powerful tool for serious investors. Cash buyers like Home Sweet Home Offers can work within these tight timelines.

- Installment Sale: Structure the sale so you receive payments over several years, spreading out the tax liability.

Whether you're dealing with selling rental property Cleveland or experiencing Cleveland landlord burnout, knowing your tax situation is key to making a clean break.

Ohio State Taxes on Home Sales

While federal taxes get most of the attention, you also need to account for Ohio's rules. Fortunately, they are much simpler, but they will impact your bottom line.

Ohio Income Tax on Capital Gains

Ohio doesn't have a separate capital gains tax. Instead, any taxable profit from your home sale is treated as ordinary income. It's simply added to your other earnings for the year and taxed at Ohio's standard rates.

2026 Ohio Income Tax Brackets (Simplified)

- 0% on the first $26,050

- 2.75% on income from $26,050 to $100,000

- 3.5% on income over $100,000

Ohio Example Calculation

- A Cleveland landlord sells a rental with a $50,000 capital gain.

- Their other taxable income is $75,000.

- Their total Ohio taxable income becomes $125,000.

- The $50,000 gain will be taxed at a blend of the 2.75% and 3.5% rates, resulting in roughly $1,500 to $1,750 in Ohio state tax.

Real Estate Conveyance Fee (Transfer Tax)

This is a mandatory tax paid at closing, almost always by the seller. It’s a one-time fee for transferring the property title.

- In Cuyahoga County, the total rate is $4.00 per $1,000 of the sale price (0.4%).

On a $150,000 home sale in Cleveland, the conveyance fee would be $600. This amount will be deducted from your proceeds on the final settlement statement.

What Ohio Does NOT Tax

- No Inheritance or Estate Tax: Ohio eliminated this tax in 2013, which is a relief for those selling inherited properties.

- No City "Sale" Tax: Cleveland and its suburbs do not charge an additional city-level tax on the real estate transaction itself, though local income taxes may apply to your overall income.

Knowing about conveyance fees and state income tax, in addition to ongoing costs like property taxes Cuyahoga County, gives you a full picture of the costs of selling.

Inherited Property – Special Tax Rules

Inheriting a property, whether in University Heights or Lorain, brings a mix of emotions and responsibilities. Many heirs, especially those living out of state, find the process overwhelming and just want to sell the property quickly to settle the estate. Fortunately, the tax rules for inherited homes are incredibly favorable.

The Stepped-Up Basis Benefit

This is the most important concept for an inherited property. When you inherit a home, your cost basis is "stepped up" to the fair market value of the property on the date of the original owner's death.

This simple rule can erase decades of appreciation, virtually eliminating your capital gains tax liability.

Example:

- Your mother bought her Cleveland home in 1985 for $45,000.

- She passed away in 2025, when the home was worth $175,000.

- Your new "stepped-up" basis is $175,000.

- You sell the house in 2026 for $180,000.

- Your taxable gain is only $5,000 ($180,000 – $175,000), not the $135,000 it would have been otherwise.

Timing is Everything

Because of the stepped-up basis, selling an inherited property soon after you receive it often results in little to no taxable gain. The sale price is likely to be very close to the fair market value at the time of death. This is a powerful incentive for heirs who don't want the responsibility of becoming landlords or managing a vacant property from afar.

Gift vs. Inheritance: A Crucial Distinction

It’s generally much better from a tax perspective to inherit a property rather than receive it as a gift before death.

- Inherited Property: Gets the advantageous stepped-up basis.

- Gifted Property: You receive the donor's original low cost basis (a "carryover basis"), which could lead to a massive tax bill when you sell.

If you find yourself responsible for selling inherited house Cleveland or are navigating the complexities of selling house in trust after death, understanding the stepped-up basis is your greatest financial advantage.

How Your Sale Method Affects Your Bottom Line (Not Your Taxes)

Whether you list with a Realtor, sell it yourself (FSBO), or choose a direct cash buyer, the fundamental tax rules remain the same. The IRS calculates your gain based on the sale price and your cost basis, regardless of how you got there.

However, the method you choose dramatically impacts your net proceeds and the stress involved.

- Traditional Sale with Realtor: You pay agent commissions (typically 5-6% of the sale price) and often cover other closing costs. These costs reduce your final cash payout but do not directly lower your taxable gain in the way capital improvements do.

- Cash Buyer Sale (like Home Sweet Home Offers): The tax treatment is identical. However, there are no agent commissions, meaning the offer you receive is closer to what you'll pocket. A fast, as-is sale also eliminates the cost and hassle of repairs and staging. The sale price is still reported to the IRS via a Form 1099-S, just like any other sale.

- FSBO Sale: You save on commission, but you're responsible for all the marketing, paperwork, and legal compliance.

What Actually Reduces Your Taxable Gain?

Remember, only certain costs directly lower your taxable profit.

These DO reduce your taxable gain:

- A higher cost basis (original price + capital improvements).

- Selling costs like transfer taxes, title insurance, and attorney fees.

These do NOT reduce your taxable gain (but do reduce your cash):

- Agent commissions.

- Repairs made to get the house ready for sale.

- Staging costs.

For many homeowners facing a time-sensitive situation or who own a home needing significant repairs, understanding how to sell without real estate agent and get a fair cash offer provides a clear path forward without the extra costs and complications.

The Net Investment Income Tax (NIIT) – An Extra 3.8% Tax

For most Cleveland sellers, this tax won't be a concern. However, for high-income earners or those selling valuable investment properties, it's something to be aware of.

What is the NIIT?

The NIIT is an additional 3.8% tax on net investment income, which includes capital gains from real estate sales. It only applies if your Modified Adjusted Gross Income (MAGI) is over a certain threshold:

- Over $200,000 for single filers.

- Over $250,000 for married couples filing jointly.

When NIIT Applies to Home Sales

The 3.8% tax applies to:

- Gains from a primary residence sale that are ABOVE the $250k/$500k exclusion amount.

- All gains from selling rental or investment properties, if your income exceeds the thresholds.

Cleveland Reality Check

The combination of Cleveland's median home prices and typical income levels means the NIIT rarely affects the sale of a primary residence here. It's more relevant for landlords selling large rental portfolios or investors cashing out multiple properties in a single year. If you're an investor worried that your rental property losing money, this potential extra tax is another factor to consider when planning your exit.

Tax Planning Strategies for Cleveland Sellers

Being proactive is the key to minimizing your tax burden. Here are a few practical strategies to consider as you prepare to sell your Cleveland home in 2026.

Time Your Sale Strategically

- Watch the Calendar: If possible, sell in a year when your other income is lower. This could help you stay in a lower capital gains tax bracket.

- Meet the 2-Year Mark: If you're close to meeting the 2-year ownership and use requirement for the primary residence exclusion, waiting a few extra months could save you thousands in taxes.

Document Everything Meticulously

- Capital Improvements: Keep every receipt, contract, and permit for major upgrades. Create a spreadsheet to track these costs over the years. This is your best tool for increasing your cost basis.

- Proof of Residence: Keep records that prove the home was your primary residence, such as utility bills, voter registration, and driver's license records.

Work with a Tax Professional

We understand that this can be complex. Consulting with a CPA or tax advisor is a smart investment. For a few hundred dollars, they can help you navigate your specific situation, ensure your calculations are correct, and potentially save you thousands on your tax bill.

For sellers on a tight timeline, worrying about how long to sell house Cleveland can add to the stress. A simple cash sale can provide the certainty you need to execute your tax plan effectively.

Frequently Asked Questions – Cleveland Home Sale Taxes

Do I have to pay taxes if I sell my Cleveland house?

For most people selling their main home, the answer is no. If you've owned and lived in the house for at least 2 of the last 5 years and your profit is under $250,000 (single) or $500,000 (married), you likely won't owe any federal tax. You will owe tax if you're selling a rental property or a flip.

Do I pay taxes on the full sale price?

Absolutely not. You are only ever taxed on the gain (your profit), which is the final sale price minus your cost basis (what you paid plus the cost of major improvements).

Does selling to a cash buyer change my taxes?

No. The tax rules are exactly the same whether the buyer gets a mortgage or pays cash. The IRS is concerned with your profit, not how the buyer paid for it. A cash sale simply makes the process faster and eliminates commissions and repair hassles.

When do I owe the tax?

The tax is not paid at closing. It's reported on your income tax return for the year of the sale. If you sell in 2026, you'll report the gain and pay any tax due by April 15, 2027. If you expect a large gain, you may need to make estimated tax payments.

Can I deduct my real estate agent's commission?

Commissions and other selling costs (like transfer taxes) are subtracted from the sale price when calculating your gain. So, while not a separate "deduction," they do reduce your taxable profit. To get a clear idea of your net proceeds, see our breakdown of what sellers actually walk away with.

Get a Clear, Simple Solution for Your Cleveland Home Sale

We know that navigating taxes is just one piece of the puzzle when you're selling your home. Whether you're dealing with financial hardship, an inherited property, or you’re just a tired landlord ready to move on, you need a solution that is simple, fast, and certain.

At Home Sweet Home Offers, we provide that clarity. We are a local Cleveland company that buys houses in any condition across Northeast Ohio.

- No Commissions, No Fees: The cash offer we make is the amount you can count on.

- Sell As-Is: Don’t worry about repairs, cleaning, or inspections. We handle it all.

- Close on Your Timeline: We can close in as little as 7 days, or on a date that works for you.

You can move forward with confidence, knowing your sale is secure. Let us help you take the next step without the stress.

Get your free, no-obligation cash offer today. Call us at 216-200-8010 or get a cash offer online to see how it works.