It often starts with a single phone call or an unexpected trip to the emergency room. One minute, life in your Cleveland home feels under control. The next, you’re staring at a mountain of medical bills that threatens the very foundation you’ve built. For many homeowners, a personal health crisis has a nasty way of becoming a financial one, fast. Suddenly, you're dealing with aggressive debt collectors and the terrifying possibility of losing your property.

We understand how overwhelming this is. At Home Sweet Home Offers, we've helped many Cleveland-area homeowners navigate this exact situation. You're not alone, and there is a way forward.

The Financial Shockwave of a Medical Crisis

A sudden medical emergency is like a shockwave, sending ripples through every corner of your life. Your first priority is, of course, getting healthy. But the financial aftershock can be just as devastating, especially for homeowners in communities like Parma, Euclid, and Lakewood. It's a cruel twist of fate: the one place you should feel safest becomes the asset you might have to give up to find relief.

Most families are already running on a tight budget. Even with decent insurance, the out-of-pocket costs for treatments, hospital stays, and prescriptions can quickly spiral into the tens of thousands. If you don't have good coverage, the situation becomes catastrophic. It’s a sobering reality that medical emergencies without insurance can ruin you financially and put everything you’ve worked for on the line.

From Health Crisis to Housing Crisis

When you don’t have a massive emergency fund sitting around, those bills force impossible choices. Do you drain your retirement accounts? Rack up high-interest credit card debt? For many folks in Cleveland and nearby areas like Garfield Heights and Maple Heights, the equity in their home starts looking like the only lifeline.

This is how a health problem becomes a housing problem. It usually follows a predictable, stressful path:

- The Initial Debt: The first wave of bills hits, and the numbers are often way more than you can handle.

- Collection Efforts: Before long, unpaid accounts are sold to collection agencies, and the relentless calls and letters begin.

- Legal Action: If the debt remains unpaid, creditors might file a lawsuit to get a legal judgment against you.

- The Threat to Your Home: A judgment gives the creditor the power to place a lien on your property, tying the medical debt directly to your house.

This cycle is incredibly stressful, making it hard to see any light at the end of the tunnel. It’s easy to feel trapped.

This is often the point where looking to "sell my house fast Cleveland" goes from a distant "what if" to a very real solution. It becomes a way to regain control. At Home Sweet Home Offers, we get it. We offer a straightforward, compassionate way to help you through it.

How Unpaid Medical Bills Threaten Your Property

That unpaid medical bill sitting on your kitchen counter might feel like just another piece of paper, but in Ohio, it can become a direct threat to your home. Think of it like a creditor planting a flag on your property—a claim that says, "We get paid before you can do anything with this house." This isn't just a scare tactic; it's a very real legal process that turns a healthcare problem into a real estate crisis.

The journey from a hospital bill to a foreclosure sign in your yard doesn't happen overnight. It follows a specific legal path. For homeowners in Cleveland, University Heights, or Lorain, understanding this timeline is everything. It's the window of opportunity you have to find a solution before the situation spirals out of control.

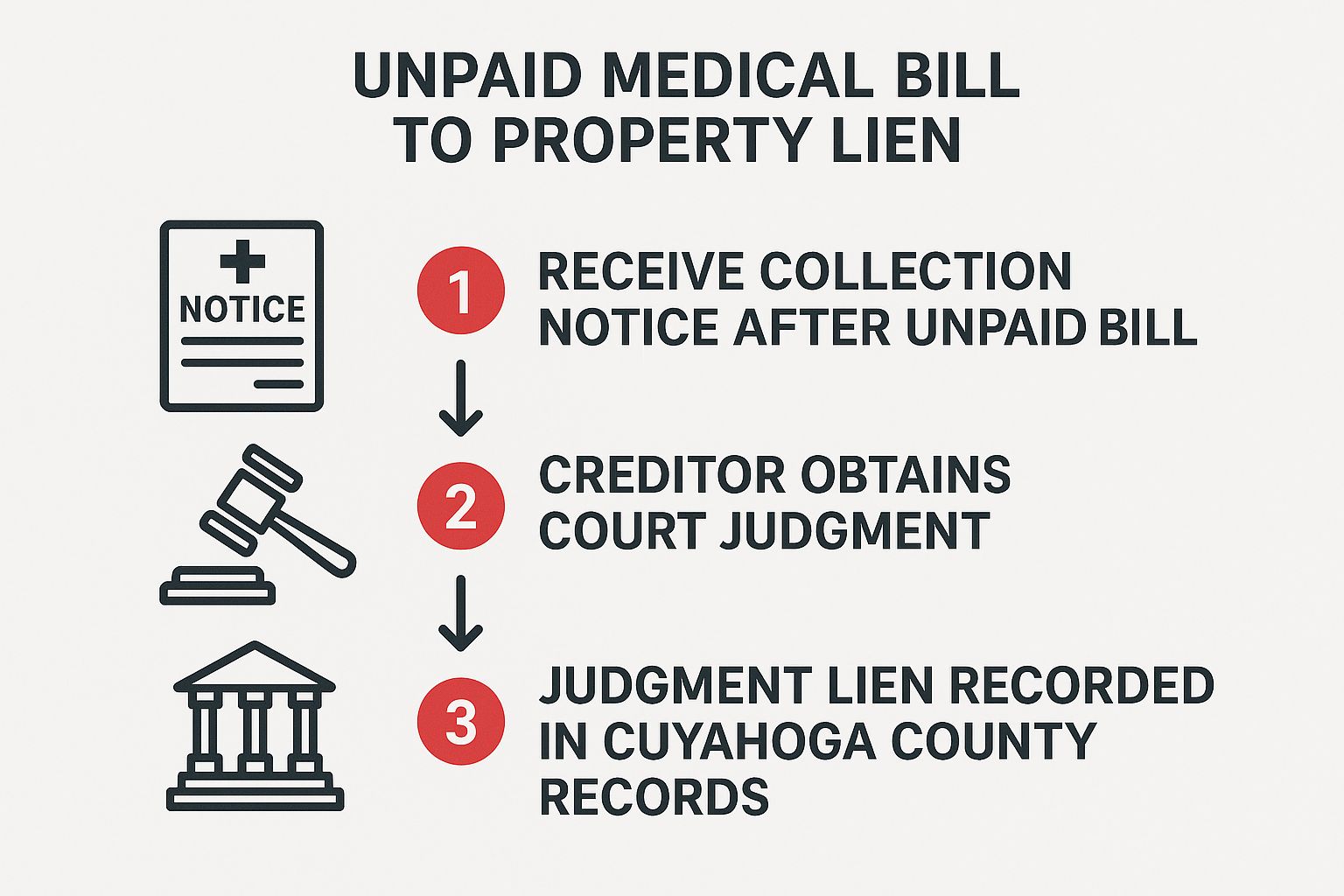

The Path from Unpaid Bill to Property Lien

It all starts when a medical bill goes unpaid. After a few attempts to collect, the hospital or provider often sells the debt to a collection agency. This is usually when the heat gets turned up—the phone starts ringing off the hook and the letters pile up.

If their collection efforts don't work, the creditor can take a crucial next step: filing a lawsuit. This isn't a foreclosure action just yet, but it’s the move that legally connects the debt to everything you own. A lot of homeowners are caught off guard by how quickly this can escalate, especially if they've been trying to negotiate or are just plain overwhelmed.

A medical judgment lien doesn't force an immediate sale, but it effectively freezes your ability to access your home's equity. You cannot sell or refinance your home without first paying off the debt tied to that lien.

This legal maneuver is what officially puts your home on the line. Once the creditor wins the lawsuit—which often happens automatically if you don't respond—they get a judgment. This court order is then filed with the Cuyahoga County Recorder's Office, creating a judgment lien against your property.

This infographic breaks down the typical flow from getting a collection notice to having a lien slapped on your home.

As you can see, the process is methodical. It moves step-by-step from a simple unpaid bill to a legally binding claim against your most valuable asset.

Understanding the Power of a Judgment Lien

Once a judgment lien is attached to your Cleveland home, the creditor has a powerful tool. While they can eventually try to force a sale through a foreclosure to get their money, the lien itself is often enough to guarantee they get paid. Why? Because that lien has to be settled before the property title can be legally transferred to a new owner.

This puts you, the homeowner, in a really tough spot:

- You Can't Sell Traditionally Without Paying: If you list your home with a real estate agent, the title search will immediately flag the lien. The debt must be paid out of your sale proceeds at closing. No exceptions.

- Refinancing is Off the Table: Lenders are unlikely to approve a new mortgage or home equity loan on a property that has an outstanding judgment lien.

- The Debt Keeps Growing: Meanwhile, interest often keeps piling up on the judgment amount. The longer the lien sits there, the bigger the debt gets.

For homeowners in Elyria or Bedford facing this, the walls can feel like they're closing in. You're sitting on this major asset, but the lien completely blocks you from using its value. To better manage your assets, it’s worth understanding the concept of a Medicaid spend down forecast. This knowledge can be critical when navigating the long-term care costs that often lead to these situations.

The threat of foreclosure is the final, most devastating consequence. A creditor with a judgment lien can petition the court to force the sale of your home to satisfy their debt. Recognizing the steps that lead here is the first move toward finding a way out—like a fast cash sale that can resolve the lien and stop the process from escalating any further.

The Pressure Cooker of Debt Collection

The medical bills themselves are just the first domino to fall. The real stress often begins when the collection agencies get involved. Suddenly, it’s a relentless cycle of pressure—nonstop phone calls, letters packed with intimidating legal jargon, and that constant, sinking feeling in your stomach. For homeowners in Cleveland and the surrounding suburbs like Parma or Lakewood, this isn't just about money; it’s a full-blown assault on your peace of mind.

This constant harassment is designed to wear you down. It turns your home, which should be your sanctuary, into a source of anxiety—a constant, physical reminder of the debt you owe. Every time the phone rings, your heart jumps. Every trip to the mailbox feels like bracing for bad news.

The goal of the collectors is simple: make you feel so cornered that you'll do anything to make it stop.

When Your Credit Score Takes a Hit

As if the psychological toll wasn't enough, this mounting medical debt can deliver a crushing blow to your financial health by tanking your credit score. Once an unpaid medical bill hits collections, it can send your score plummeting, effectively slamming the door on any traditional financial escape routes.

Just like that, the options you thought you had may be gone. You likely can no longer:

- Refinance your mortgage to get a lower monthly payment and free up cash.

- Take out a home equity line of credit (HELOC) to pay off the medical bills directly.

- Qualify for a personal loan to consolidate everything into one payment.

The equity you've built in your home is suddenly locked away, completely out of reach right when you need it the most. It's a story we see all too often across Cuyahoga County. Your biggest asset starts to feel more like an anchor dragging you down.

The Impact of Medical Debt on Your Financial Future

The damage from medical debt on credit reports is a massive national issue. For years, these bills have crippled homeowners' ability to manage their finances. Thankfully, local efforts are making a difference. You can read more about how Cleveland has worked to erase medical debt for its residents, but for many, the damage has already been done and the pressure is still on.

When refinancing is off the table and creditors start threatening legal action, the idea to sell your house fast in Cleveland starts to feel less like a choice and more like a lifeline. It becomes the only clear path to silence the collection calls, settle the debts, and finally take a breath. This is especially true when you understand how quickly things can escalate—learning about the foreclosure process in Cleveland makes it clear why acting fast is so crucial.

Selling your home becomes more than just a financial transaction; it’s a strategic move to reclaim your peace of mind and prevent a bad situation from getting much, much worse.

For many homeowners, that relentless pressure from debt collectors is the final push. A quick, clean sale with a cash home buyer like Home Sweet Home Offers represents a definitive end to the harassment. It’s a way to wipe the slate clean, pay off the creditors, and walk away from the stress for good.

Why a Traditional Sale Often Isn't the Answer

When you’re staring down a mountain of medical bills, the traditional real estate market can feel like it’s working against you, not for you. The whole process of listing with an agent is built for sellers who have plenty of time, extra cash for repairs, and the emotional energy to spare.

Frankly, those are three things you just don't have when a financial crisis hits. If you're a homeowner in Maple Heights or Euclid needing to satisfy creditors yesterday, waiting months for a sale that might not even happen isn't just frustrating—it's impossible.

The conventional path to selling a house is littered with hurdles that only add to your stress.

The Roadblocks of the Traditional Market

Putting your Cleveland home on the open market means navigating a series of major challenges. Each one costs you time and money, turning a tough situation into a nightmare.

- Expensive and Time-Consuming Repairs: Most buyers want a perfect, move-in-ready home. That often means you’re on the hook for thousands of dollars in repairs before you even list. Whether it's fixing a leaky roof on your Bedford colonial or overhauling a dated kitchen in Lakewood, that’s money you may not have.

- The Disruption of Showings: Living in a home that's for sale is exhausting. You're constantly having to keep the place spotless, shuffle the family and pets out the door on short notice, and let strangers traipse through your life. It's a huge disruption on top of all the other stress you're managing.

- The Uncertainty of Buyer Financing: Hearing the words "the buyer's financing fell through" is every seller's worst nightmare. You can wait weeks, even months, only to have the deal completely collapse at the last second. Then you’re right back at square one.

- Hefty Realtor Commissions and Fees: A traditional sale comes with a big price tag. Realtor commissions will slice 5-6% right off the top of your final sale price. On top of that, closing costs can gobble up another 2-4%. That’s a huge chunk of money that won’t be going toward your bills.

These obstacles reveal a fundamental problem: the traditional market requires patience and a financial cushion, while your situation demands speed and certainty.

Why Speed and Certainty Are Critical

When medical debt collectors are calling, every single day counts. They aren't going to pause their efforts while you renovate a bathroom or wait for a buyer’s mortgage to get approved. The pressure is on, and you need a solution that matches that urgency.

The traditional selling process is a marathon filled with hurdles. When medical debt is closing in, you need a sprint to the finish line—a direct, guaranteed sale that puts cash in your hand when you need it most.

For a lot of homeowners, those commissions and fees are a massive concern. It's so important to know exactly how they'll affect your final payout. To see a clear breakdown, check out this guide on what Cleveland sellers actually walk away with when selling to a cash buyer versus listing. The difference can easily be thousands of dollars—money that should be going toward settling your debts and getting your life back on track.

Ultimately, the traditional real estate market is designed for people in ideal circumstances. When life throws you a major curveball like a medical crisis, you need a different game plan. You need a process built around your needs—one that offers a fast, simple, and guaranteed way to sell your house as-is and finally move forward.

Finding Relief with a Fast Cash Home Sale

When you're drowning in medical debt, the constant pressure can make you feel like you've lost all control. Traditional solutions often feel too slow or just out of reach. This is the moment where you can take that control back. Selling your house for cash offers an immediate, powerful solution—a direct path out of the crisis.

The process of selling to a cash buyer is designed to cut through the noise and get you results when you need them most. Unlike a traditional sale that can drag on for months, a cash sale is built for speed and simplicity. It’s all about turning your home's equity into usable cash—fast.

Taking Back Control by Selling As-Is

The most empowering part of this is the ability to sell your house as-is in Cleveland. That simple phrase changes everything. It means you don’t have to spend a single dime or a single weekend on repairs, updates, or even deep cleaning.

Dealing with contractors and renovations is the absolute last thing on your mind right now. A cash sale lets you bypass all of that. We buy houses in any condition, which means:

- No Repairs Needed: Whether your roof is old, the plumbing is leaky, or the kitchen is a throwback to the 1980s, it doesn’t matter. We'll handle all that after the sale.

- No Showings or Staging: You can skip the endless parade of strangers walking through your home and the stress of keeping it perfectly staged for weeks.

- No Realtor Commissions: The offer we make is the cash you get. You don't have to worry about thousands of dollars in agent fees being skimmed off the top.

By cutting out these steps, you eliminate the biggest sources of cost, delay, and stress in the selling process. This puts you firmly back in the driver's seat.

The Core Benefits of a Fast Cash Offer

When you work with cash home buyers in Cleveland like Home Sweet Home Offers, the entire experience is focused on solving your urgent problems. It's a system built on three pillars that directly counter the issues caused by medical debt.

1. Unmatched Speed

A traditional sale can take 60-90 days or even longer. We can often close in as little as 7-14 days. This rapid timeline is a game-changer when creditors are threatening liens or foreclosure. A fast infusion of cash allows you to pay them off and stop legal actions cold. To get a better sense of how this works, you can learn more about why cash buyers can close so much faster than those relying on bank loans.

2. Absolute Certainty

When a buyer needs a mortgage, there’s always a risk their financing will fall through. A cash offer completely removes that uncertainty. Because we use our own funds, the sale is guaranteed. Once you accept our offer, you can be confident that the deal will close on the agreed-upon date. That certainty is priceless when you need to resolve your financial situation without fail.

3. Total Simplicity

We handle the paperwork, the title work, and all the tricky parts of the transaction. Your only job is to review our fair, no-obligation offer and decide if it’s the right move for you. It’s a straightforward, stress-free process designed to bring you relief, not add to your burdens.

Your Path to Financial Freedom

Medical debt is a huge problem, and Cleveland is no exception. It’s a financial threat that pushes families into heartbreaking situations. In Ohio, about 9.1% of adults reported having medical debt between 2019 and 2021, a number that's higher than the national average. You can learn more about local efforts to erase millions in medical debt, which shows the scale of the problem in our community.

A fast cash sale isn't just a transaction; it's your strategic exit from financial distress. It provides the funds you need to wipe the slate clean, pay off every last medical bill, and reclaim your peace of mind.

This isn’t about just getting by—it’s about moving forward. The funds from the sale can satisfy judgment liens, stop foreclosure proceedings, and end the harassing calls from collectors for good. It's a powerful step toward financial recovery and a brighter, debt-free future for you and your family.

Your Options in the Cleveland Community

When you’re staring down a mountain of medical bills, it's incredibly easy to feel like you're completely alone. But you’re not. This is a massive issue, and thankfully, leaders in the Cleveland community have recognized the struggle and taken steps to fight back.

Knowing what’s happening locally gives you a better vantage point. While community programs offer a ray of hope, they aren’t always the immediate, one-size-fits-all solution a homeowner in crisis needs.

Cleveland's Fight Against Medical Debt

In a huge move to back its residents, the City of Cleveland got proactive. In 2023, the city set aside $1.9 million from federal COVID-19 relief funds, teaming up with the nonprofit Undue Medical Debt. The results were staggering. This one initiative wiped out over $165 million in medical bills for more than 161,000 Clevelanders.

That’s an average of $1,024 erased per person. For a deep dive into the program's impact, you can learn more about Cleveland's medical debt relief program here. It was a lifeline that gave thousands of people a fresh start.

It's a fantastic testament to the city's commitment. But as incredible as these programs are, they have some practical limitations for a homeowner in your shoes.

When Community Relief Isn't Enough

City-wide debt forgiveness is a powerful tool, but it doesn't solve every problem for every homeowner. Let’s be realistic about why it might not be the right answer for your specific, urgent situation.

- It’s Not Immediate: These large-scale relief efforts move slowly. If you’re already getting foreclosure notices or dodging creditor calls, you simply don’t have the luxury of waiting to see if your debt is chosen.

- The Debt Amount Might Be Too High: The average amount forgiven was just over a thousand dollars. That’s helpful, but if your bills are in the tens of thousands, it might not be enough to stop a creditor from placing a lien on your home.

- There's No Guarantee: You can’t apply for these programs. Your debt either gets selected for forgiveness or it doesn’t, and you have zero control over that process.

This is the point where you have to shift from hoping for a rescue to taking charge yourself. You have the power to solve this on your own timeline.

Community support is a valuable safety net, but a direct cash home sale is a powerful tool you control. It offers a definitive, immediate solution to regain your financial footing without waiting for outside intervention.

Think about it: a fast cash offer gives you a concrete way out. For homeowners in Cleveland, Parma, or Lorain who are out of time, it puts you back in the driver's seat. You get the funds to pay off creditors completely, get liens removed, and finally end the constant stress.

When you choose to sell your house as-is in Cleveland, you’re creating your own relief package—one that’s perfectly tailored to what you need, right now.

Common Questions About Selling Your Home Due to Medical Debt

Facing this kind of pressure brings up a ton of questions. We want to give you clear, straightforward answers so you can understand your options and feel more confident about the path forward.

Can a hospital put a lien on my Ohio house for unpaid bills?

Yes, they can. While it's a scary thought, it is a real possibility. If a hospital or other medical provider takes you to court over the debt and wins, they get a court judgment. With that judgment, they can file a lien against your property with the county.

A lien is a legal claim attached to your home's title. It means the debt must be paid off from the proceeds whenever you sell the house. This is where selling for cash can be a lifesaver—it allows you to pay off that lien quickly and stop any further action, like a potential foreclosure, dead in its tracks.

Will a fast cash sale truly solve my debt problems?

For many homeowners, it’s a powerful and direct solution. A cash sale provides a large, immediate sum of money, giving you the ability to pay off medical creditors, silence the collection calls, and clear any liens. It’s a clean slate—a chance to move forward without the weight of that debt or the constant threat of losing your home.

This approach gives you back control, especially when other options like refinancing are off the table because your credit has taken a hit. It’s a strategic way to resolve the crisis on your own terms.

A quick home sale in Cleveland is more than just a transaction; it's a definitive step toward financial recovery, giving you the resources and peace of mind to rebuild.

How quickly can you buy my Cleveland house?

The entire process is built for speed. When you reach out to a company that says, “we buy houses Cleveland,” you can often get a fair, no-obligation cash offer within 24 hours.

If the offer works for you, the closing can happen incredibly fast—sometimes in as little as 7 to 14 days. Or, if you need more time, we can work on your timeline. That speed is so important when you have creditors breathing down your neck and you just need a reliable way out.

When medical debt has put your home on the line, you need a partner who understands—someone who can offer a clear, fast, and compassionate solution. At Home Sweet Home Offers, we provide fair cash offers to help you resolve your financial challenges and move on with your life.

Ready to see how a no-obligation cash offer can help you? Get your free offer today.